From digital wallets to biometric authentication, the future of financial exchanges is set to become more integrated and efficient, according to global payment technology company Mastercard.

A new Signals report from the company focuses on the future of payment systems, identifying seven key trends set to shape the industry by 2030. Experts at Mastercard envisions a future where payments are faster, more secure and seamlessly integrated across platforms, borders, and industries, as luxury brands continue to embrace a wider range of digital solutions.

“The challenges ahead are as significant as they are exciting,” said Ken Moore, chief innovation officer at Mastercard, in a statement.

“Success belongs to those who not only have a keen eye on the road ahead, but also the agility to adapt to a fast-changing environment,” Mr. Moore said. “It’s a team endeavor more than ever before.

“By embracing innovation, navigating complexities and prioritizing inclusivity, we can accelerate toward a future where payments drive global prosperity.”

For the report, Mastercard examined the global forces and new behaviors influencing commerce and payment systems, referencing internal research and synthesizing insights from accredited external sources.

Roadmapping the payments race

The way consumers and businesses exchange funds is undergoing a rapid transformation.

In the lead up to 2030, one of the most significant, its authors outline, will be global interoperability.

Throughout the report, motorsports analogies underscore each trend, stating, for instance, that “much as motorsports features a variety of tracks, each with its own challenges and demands, so [too does] the payments landscape, [presenting] a dynamic maze of different systems.”

It lists current roadblocks for account-to-account (A2A) and real-time payments (RTP), two tools that consumers, business and governments alike are looking to optimize for smoother operations.

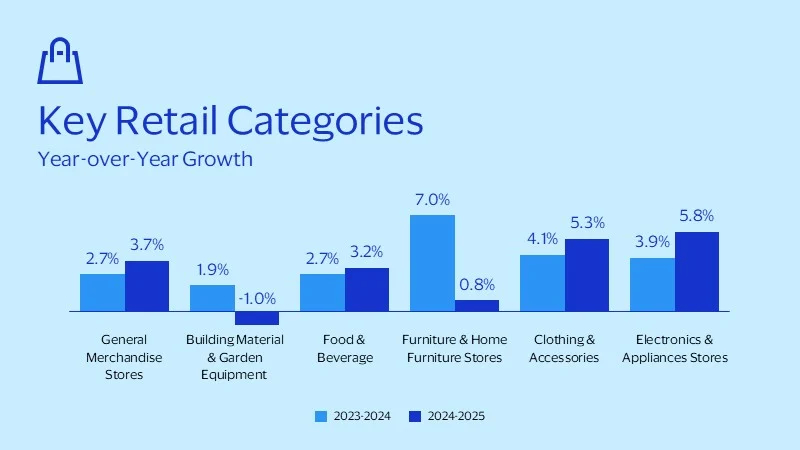

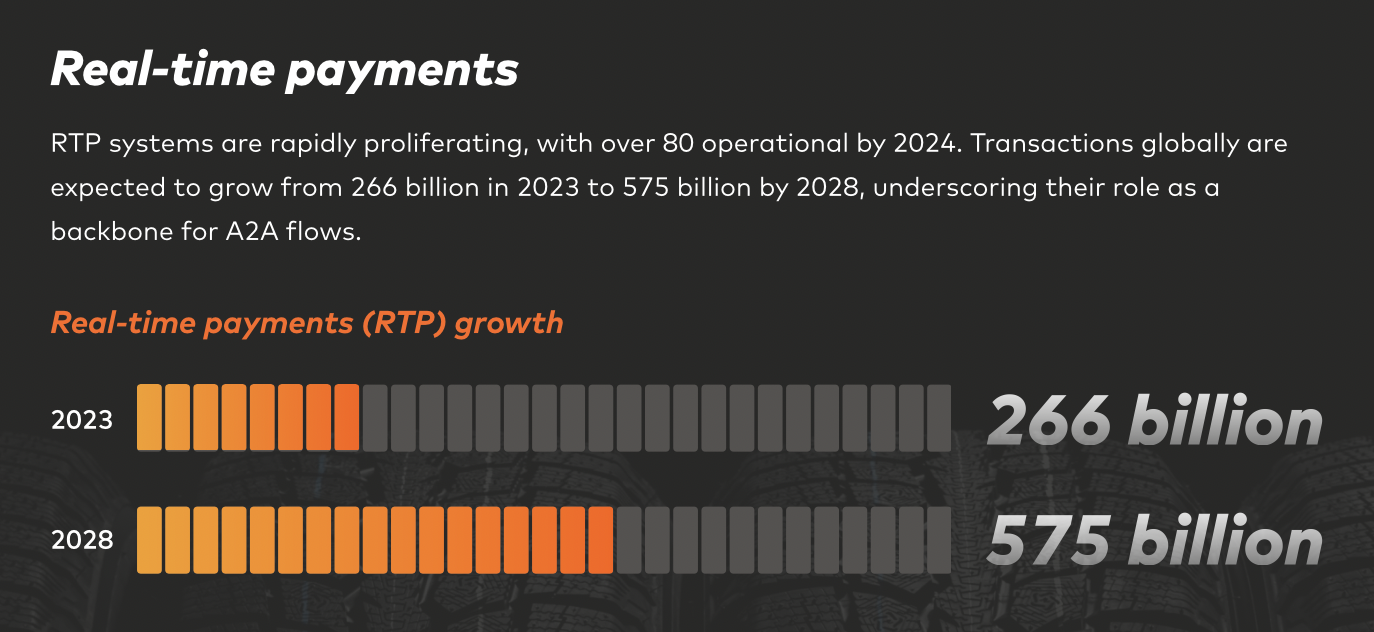

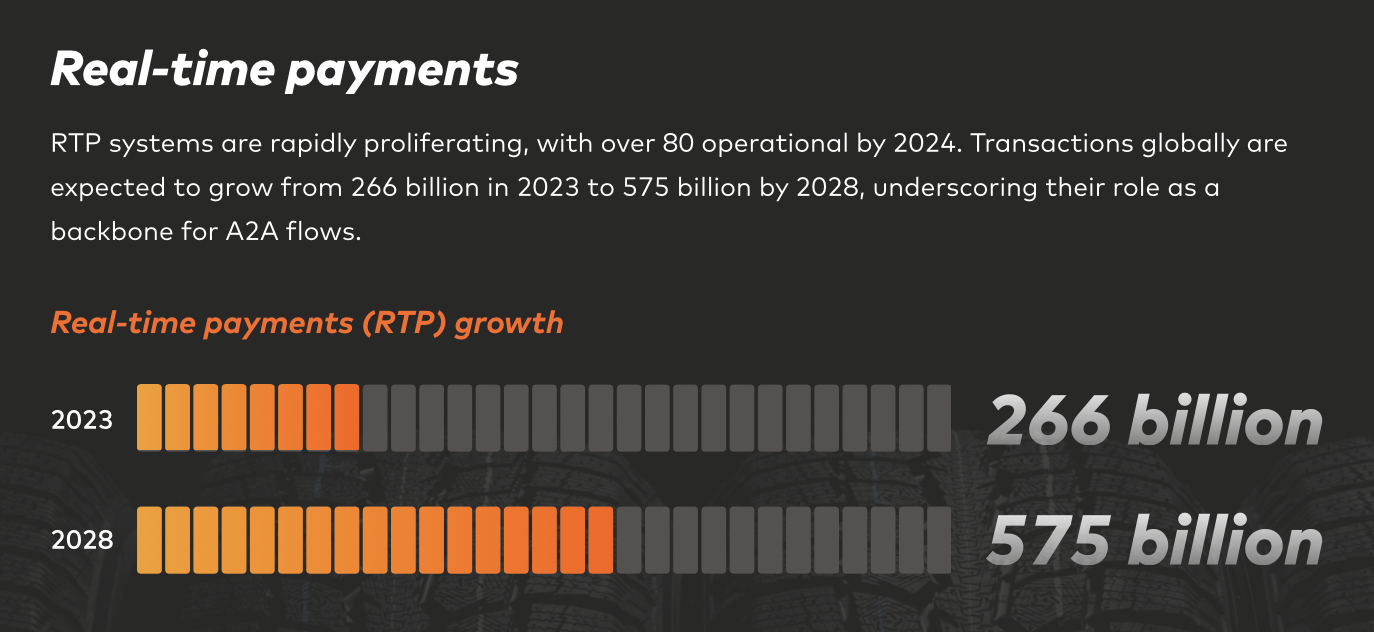

According to the report, RTP systems are growing quickly, “with over 80 operational by 2024,” its global transaction value expected to grow from $266 billion in 2023 to $575 billion by 2028, aiding A2A convenience.

The global transaction value of RTP tools is expected to grow from $266 billion in 2023 to $575 billion by 2028. Image credit: Mastercard

The global transaction value of RTP tools is expected to grow from $266 billion in 2023 to $575 billion by 2028. Image credit: Mastercard

Alternate payment methods, or APMs, referring to any payment method outside of traditional credit and debit cards including mobile wallets – Apple Pay, Google Pay, Paytm and WeChat all qualify – and buy now, pay later providers such as Klarna, Affirm and Afterpay are additionally thriving, granting shoppers increased flexibility.

The popularization of digital currencies, which enhance the traceability of A2A transactions, is also welcome.

These solutions carry the potential to help eliminate friction in cross-border and cross-platform transactions in the near future, allowing payments to flow effortlessly across different currencies and systems, enhancing financial accessibility worldwide.

Still, security risks have continuously threatened progress (see story). The report cites that authorized push payment fraud losses in the U.S. are projected to rise from under $2 billion in 2022 to over $3 billion by 2027, though AI-powered security and shared standards could work to combat these threats.

“Tomorrow’s payments ecosystem must deliver the same level of security, assurance and convenience across the board — regardless of payment scheme, rails or jurisdiction,” said Peter Reynolds, executive vice president of Real Time Payments at Mastercard, in a statement.

“That is the challenge, and the opportunity, for our industry."

Interoperability, security, inclusivity

Identity authentication, digital wallets, hyper-personalized checkout experiences, embedded finance solutions, advanced fraud detection and integrated payment partnerships – boosting an ongoing fight against cybercrime, Mastercard itself recently teamed up cybersecurity and compliance firm VikingCloud, which alone serves more than five million merchants – are among the other trends expounded upon in the Signals report.

Growing by 400 percent in 2024, advances in biometrics are enabling the widespread use of passkeys, which rely on safer, more secure inputs such as fingerprints or facial recognition in exchange for access to digital accounts and sensitive user information, the technology developing substantially over the years (see story).

By 2026, the total user base for digital wallets is expected to grow from 3.4 billion in 2022 to 5.2 billion, representing more than 60 percent of the world’s population.

Research from Mastercard says that nearly two-thirds of shoppers still struggle through manually entering their card details online, with 25 percent of carts abandoned because checkout is too complex or slow. Answers to thees ecommerce issues such as Click to Pay (see story), and in-store solutions including Tap on Phone, allowing for contactless card or digital wallet payments, are increasingly ubiquitous, saving shoppers time.

These are just a few of the insights supporting the report’s findings. Mastercard argues that these trends are not evolving in isolation but are, rather, collectively driving a future defined by interoperability, security and inclusivity.

{"ct":"ehK+aliRgGc0mR2TO\/p5ZwqLNtWcEApbA1x6DQggHE7dm3ZGymttrYz7IBT88koRZHB3Ece7g4jhEVcF6LUEFrJaEPQK8zqnexlsboBrnev1I4eio5lipOUIx13BN9nTL4SY9q8CD\/j\/f6vJr5U6b4ov0gJ+5bqXM3nMuipQq0iwO9n7ybqAI5umuEA8A+4J88vxtd9QS4+77Q1RoiALpqMkarzLhd3bEPgwLKX8gw\/xnBTgJ7xAoZpLtbeUfSDzBnSTsik8K0\/usVHBOxQZE1p4\/O92sPUkIcQneb2jN2meRGPVYVWKY\/skEmW112UtxJ8NT7F4sfjkaNOQPYDeod0UWRzIgl3Goz+DEbwSQJe0YuwO2UcZ3jzsqZvtaQsfHiI40iMnx2IIywUvOadpexROYaQT023CJKhtHEBPmdybDpZUbkdXSNelBYUpe4TM12fo2VZCMZBlx5Xseop272Rpe7oD0RZ7Z4V26V4TdcT7cQn693Ap4Esw6H3k2Q9ZnHaln9gQGK6E+QGZRUv6QrPHY89CDgTjw0\/FRtbJcMnGowyS\/GMq5Rq0GRSDeDTgJ\/MYOX7j7djvglUtgcEhim0MfVIcPOsGqcqrXFDbHP4sWiWO2thsb7S+C9GjVHFHQBcpirhAeQODmyC5\/DRLelRQ9XiQKYiyTmGpuYDlIxglOZ+L8ttv+0JGK\/la1sd5dICpboxvKpn7Cb\/xzOGXTINJVDTvfR5NslMJuBQyorC3bZmi+Pb5iJf3uJDfprT\/pF2YzLTfdueXKB\/JEhJICmX9SG08Rt\/8HpzNuRormO6m1JgmuhTBGfNoH\/iazoL\/mHz\/YF8Heyeh1MQG3h5ve7CtQ8U1XFm7fBX56vLDZTv99SCT1S2zes3FrC9jqvwfBWbvsdO0rc1Kcj9cNPQrXVyD1XACjnS6AQErEiuEDsZur7cGnYnM+n0C8MKtxGIgaNI9yRCXO6zWyh5aFt6kkyP+NXI5R\/bKff0shlhRaL+bzlLZqIyjssnoxPON8ZR+Gck1ETu+mnEgdtRdO6zGhFdhcNnqYNs5a0mt1C93\/x1NpFdoKqU4GKYtZIkUnIX5BjF6fJUDZQIsLg+5IeEUO0nbGkqLQE0sl\/aLjvWov11TA4rH48BJdqpV9LWlIhWUAcw0ayWU3nGdRK9j2sW4L\/e4Q0hjhf\/OM4V32LFwPVtOc4aBPCyQF0pEKzXyt8BcwUTEIYTNn\/9e86u3RLXdBJkLYDLtL86x+P2kBcXREOVEU0+eyXZfsgJKBvznm0nzWiwJ\/1ZRtfkTTMnoAQgKvbYQljXkbc4MLf\/O0aBgYksO+IIdOVI3tOLm6DnbGicj7hcWrkORFN\/jBxt5LfnoVfEJZaB\/ARzv94iuY\/Lsnh+Z8KPPn2nWYhK+X+qFoDbTL17i\/gzqDNhrctjem2LmyPqF\/nwOgMOlnUa+f+bsltZC53MhX4R2ymTxA29PtTsYBY0KzH9mXj5Yk026rsYy9PXDgiMpu271D\/hWjLUPuTWMT7DJRG3Cjb1NDLJSUjNcbNmv56DC6jXsmxng7S4AOFs8EfxXooqOYfKSw3eh0WKfiqAaiIN6dj2APjDaBaoS+iuxS2Vk+njIOoaQtbaM8uUqiCcCLc81Fve7JTg5RxTRVnupoJSQAfFN1GCbIrMcLvcdxwSizSkl6QWfs3NhqW4wjJblotqnGKv+CFnzLfcRGlIH6WLthGa0hSrr62Le9wibxzf6lXGen\/+cowroA3QXph5jLRwAhaW+w1qlTX7snHqB6Q+wHOhgOUjY7QXJ9cXdbG6sOCqtMCa94ovYBD9ezqkgPpuW0ZKWKX3bJ2\/fJdvs1BQBnEfQUVl9TtXe11pzVr0F5Kf0l+ViLMWYNLKQjce4xozBpHACJrCkNYyf1ouMz\/kKHpMntSCWQyv8WZMreT\/5cNB0lnLbV1\/JHsVrkUsyXw4SZY3IS0\/75BiUY\/95gqHV9WQ6Illh1oQZHF2NquAit6nsVLfjxFKf0FsVH3aEC1JZbcloAfRrRdc7lZIRZmrezucfxgzitSMXrrnnT6gUQiEDN4BNixjn90JZcj3RWadlZDWwqLoVBzJ6E4TUYC2vl\/8seymxpHpJUjKSgdmaHvPdIQGox6lSx2bT078V1z4SKVU7yM4PxAHlB8NTnLeZwchTuWje1xfQdgZUQva\/R4Ey59An5wWH0WZy1Ja1+kjnmVaslnizJ8+ge9tPi0igB2upf5cyp+GRBiWKjosSc+XTKlaEUD0v9UWj++klZB97yMIoWRelqCYyQOhvT5DNpGY69pUsrSj56e4WZx2dx7auV+RDse1eW9xRgRD4aOBuEU83M9fJe1vs1P17b6yFgkvS1et1rbjJqbjlMhajixQIkWReRtCeVKMZ\/8E3jR9r5GUPM9bYGr83Lji3e+0h\/ElRXuJQOyNwbe74Z4VzKQA6DYbGVkl1KHs7krvjjvVSDdqGSDyxnywjoh97NHIgvnULcTfa\/k0cYKXCaEgeNZjhXDLYByXoOph2GZaWPkVJ46eKMMxGGpJ4AyStjJj4ORRHTWSF\/5P2aB4iDvUPf1DW2gu\/b6jPX6lbbuFvXJp\/lOnUPvznLMWfUlRDEBagdIFRJMmWdBOELtxbHm4lRfvRpXolChINSUHY5eZX6CukOeVO99yq5ZN59mWyDF7rFw5rDw5lAOxlweOhyESWEuZH+6gXd\/SbGqfCboVC2Eghv\/gaw0dgw9GTpq6zPJi0TXk9VoUKURJPXLTO9aQ6FuWFFsXUoO7wbowkbacJMIZR69lGJmhf4JZn9YSNsZnzf7aRhXo+AZMu9MnzrjJgeFI1CYatXKGLm+Prxdga5DTbsj1wqdWnCpIAWO5m+LdIRiQevQ5XwDGxq\/76K1MEnP9PzostVCjBSJL0go6vUeJlcFXhKpr5NSYd\/rxV3I7tTj4Zx9J\/VeMitYtf+22\/0WGzmyEVM6P1qPloW+dEmJahOKUPIFqZFNgOVOPxf5o6fmqyejZwW02SZd0zFZrUwycTzJCqCJZFop\/gR0iOOYiElSoYIjPMAnsU1\/lTIToZ4o2Yn58ry+wT5LEq8H42BIL0myVAlxLp5SsTc0vUvYuGH8SfsAKk1r+6\/iyAXVPub7N5cxAdhRo8xA09YKoPkDgPx8olupH\/pCul6osp8cVoGYKkh19ZEUHQGKvHkx8pyud7QMbNZjIEOqyjrpXoGq9yCnRC\/W8Nwv0Wqey3zM6ErrxdfNbugfRhCNlsj7u5pn1u+06tdgbbOpxAQiEucpFzD3ZSU3GEwNn+NfBn+Qef8vB\/W1AHqumPVvvoefWY1tR3wBe+HuExByjr6mvxJQ3crg0ZZ2XwhqdCkvE9XqmX8Digct1NnCRMuJyAL+amT0RtL3QLpF5n8lz4wzjZuw+pHvs+P8tThtUvFmPKU0m7MTBr4JJd6G7KJX0rbiJG0bs4Pn+c6qulb0G5U5dH2+um+Fr7r9wVyUPRcgM\/nngToiShNMPEhS7kUWAVQ3VPno7KAhe1HtYT8Scghzr4H3xnfwSdXJsYxpEE3IcklAh4JU7H5DFGMaIHhDI1m8EJLlBtTYU4LhwvflOIfitNIzBtbqpjbW\/O1+MClOteEtOBaW3qY0rRsnxpkImcNDVsw+S0HpzYzUH1QZmcJlJRXzT7DtBNEdJyEui2ue0LZb9NpWGaL1S3hTWdmsEVPPVSqVEAz4VWtoQqyMOI1k+MjktN+nqnu7LzG7mv0ESCHF1hI9+8BMJycIvoH8V67zX86j7KieMl+Z8BxOFAxh49e\/n8xmGUo6D\/t64j+c9HvBl7Hbc2SDEU\/w3yrz0RpOKplOsCIyDd\/cJWs39cWbYqhp+Tb5zLCPRT14yD\/patRjqz\/kxE+hSGHk637ARBdH8uEm\/FNQ5ooKvad\/rczxpPoc6LngA+2YjTCKQdp+JbGyKgJ5yInjjh+ZRDrhYef5i7dZ6m\/fgxuP4bncy3nJXZ475Lmjv7a46FYddulZKHBXmj7A6NY5ZEMFArRKQben\/lMJBAr+OAxDSE1GYOUldKdsVWP4lpNCJflBOM779aDI1YBeejnluHfp5HX4JIWr4\/i5\/UBJbfOoijONZvVj1Cp80GtfIbFNmqzrNY1UUDn6EHHygTk3YjMJjybo679hCqESlwwm6jOuB3ySOFKMshBi9GUUrGY8D7JCzfXsLFrcFEjCqkyCJRe+PkA4UScm0XqoeX8sjifY4BSs2CtDDuNiNB9AYpHIwF3OFnZgulVuHq54fB1BDSGFuhd33wQ5D7+NmlHLR3OndKEwedxJm43iC7kdqcDu7aJ+2ox2dFOcSQJAHj3qwmQ2WEXruXMHIiE3bvyxRWzDUVJHD6CJwK0a\/EV7V2P7D3YqMT1Qdw4xwl1um+3NBz6JSguu6yugHgSNh5Q0HYCuiy84B0XkFAn5RlSndeJgwSdynZadqxwkYCjvPDm7BOW46IQ8Zs0GQlg6qTT8gyB\/Aar+g1b54O\/BziZHnvFYdS3fgJnFd8Mj1q138sxiFj\/vL4716f0Mcx+ciGt00b98DKlI5tYgivVprhxN3+tCbz0dgDj7ROXM3GWw1FvWWOfEP\/\/RpGMQFA2fghn3xWECMlxNTRG2\/3zD1KBZ8wTgi8nNKF4ElxMNyfNsVlPzElF6PQ\/dL4Wgymx2+RMdQ\/fdQyIuQc6HcFkvGfScIVcDdqPWQ8o+pzaxZQV2Jj59+DoShE4UYK0Rr8gI8CYNxA9e3AfhlkdvJyZ+I8s13SpJkQIPihwdabgTRbmTsSMaKAZtO5uGnrVXsqZrc56Bbl\/aE2zbtN+t9l5YeN7kyby5Apvy8serblCt2cU5ILlrSJ7vwI8pmdE+opqAUhXa2F2AwW3IvBilPZhVOvviHMOo6Vx3lDExmMRf9RfiaeDKbNBzMTOF8ZoDpzY5BLipp\/OFhZSyARryxGD4jqaZ9uXANNZtpQ37EMFi8l6ATwz2c57AkS84NeXTlSAlvJHyuaGJW2jGBnhRTzObg8AxexYUTefIPXclo7qiXPE3RPlrrmEbn2ZvbTkYp9397Jhd6Ho3oT\/viUepycKPv9KlHdnpEn5ttfKD6D0LSpCwS+PVlUZriUGfBSylF\/zg4oj\/SSjj3y\/axI7RzHsdoqNmwK0FBuUs2HqFT8FyEShjubzsmYr8dYqGaQ08fTrv53nRdJFWwj8QXnAkXGJEq\/abBUkQqHoZGJHGynhMwjsTaCZiQfXAJDukCW0T2aK8xod28+K69BFjGZnAxknB6Sf0577hxfsCbLzC3PfQT92q78KQdvUH6Khr6gG74gN86qryjtlh7oI8b29OEE8gZxPigwh4AWv+5rstq\/CjwRSfF37HwsYNkt4RjoRTUAUQI5RrMBBFGn859IBHOz0M25f2dOexTsspsP\/zQ4PXhvvqieToeBN21L32P9cBY8ZWilsbCvVNQildrguLx7f\/lkju3Mp6i116qKQs89iV\/SA0TCDN9MwuLObiRDd81nVrMYd06QU58XNt95mB1nELcAi44OaSeIGs0H0ZfWFNstiidm4F3U48GVfovPSBK1h8IBf7\/iXpBZtFRdYTh5FSvpXqWJ7f75ze0FFFtgh8iKrzzugbyVHDZNtXEn5TSYraYBSrt\/1M\/sS9M1kLDBSHFnvD0cfN+9MJPtPkx2fPVl6PIAH+iZD3mXXRxGxrUuVMYhKV7nZ8aoLJMeoqFH2q\/6\/3Em6TyxJdIna5cj2JHO61jkMq6NPI1lwUSTXj4H2NVMP2r0vgRwH04+6W6Xo\/K2xXPGqLd6DaewGVNoxZSUHoMj0r6UZIxsFn6W9CZaoeW9RgQKVi7XN7tb0+6KpBOt1g3P11fVyhU5+HoIpxQzQYbo7FCd9bOK\/jcO6UATziR+DJs1gGD+mEiTjIZg6aU4WBlLe8GY7bFr1oEbiMS+00DLaz\/O6rdg4j28e2DQxEA\/86NbWr7XxPOKRZh14nFmlADDW8HFzJTrvbTLhH0vT0SPP4eKxHRqsbB8uq1\/gOqVya718Ux6NV2yLrQCbhTMY6FyaIuK6iY74ZGl+uEILUsoVEAdPPjbVcoA\/hK+yRHHeL2aulxfl\/4tznCXO150I8aFD\/scYZckx8jYHITqt8KoNJEoG0z2w+6KYS\/xS3jKq1u+wOjwTt8Vo+v0xzLC7nRD7s9BoV7XPVFw\/235oUJn58lqYIC5swS+o1c4A7wusxyoHdIlp6Sr+osR7t1rMQNU9gN2ycZhQcuzR6CUxyvJWc+eLosSB9pG4FC4b4hXWs2nX\/7cP1GdckcuK0Ce5Sj7G4NIQGhJ1YvtoU\/c++zrI24y59yl6UicGcHL9bOo9+St7XS7NO1xdNlxvRLgciX+cwHh64LREl3faOrqXdcTXp68YCN+eZB7jkc3yyeWQg1w+4sECHcWT1GmODTdT0+MRSGONk1JBnK7jrTdjBDXK60z5nrQPPjuWstOzS\/r44LWkliYjKT3jIPo\/13Itvfn+TrmLmVTDjC+B4DSGd23vH8U2wN2xIK18aiceSdnxVlfYeq4h7KGRL\/62c0d\/XsZ1AId9QVdwSz9YFEwVCzDzA3n7a51nGEJsAMhZazesOXR05VKvmptGDdXxTBzKpW1v03zFie\/yj4OM8uRZ0LPEAS0KcLXSiOXt5BXUG1rm5p03g\/JU6efDIjKNdOupFp+kY1ROmh\/q24S\/eH4qVbuUtu73Irtl0uYlUximf1k++GUZPHoTTo865yplY\/NVu69umxKBR20d\/BTLv\/yvx8uV24Zru9B3g5+GA58d50KggtQKk\/TzSL6V24Uz\/qIJPUPOiXHe9KNCn4HJUUHz0oKQPbtHoDWkYvEPVcBRtmlxYcYEuOIYpn1Fg258jsPqprVMHSzODNH4DXs2raH8RwxUSeVSVe17kvLfSWucXovGZpY3l1I3U0VxGNjUuMiz4\/LhkS8EXZ6XEL+gHjQZnSMMlMq9Hv8V19WYmTu9gyQj8O0sJSRkC69DkZKQjsHMNyCTjKJbsT9oHF8eU2R3wbpYVOwIRaCtgwZPcJKaGKOPuxJC7TJDhllYCTZ726hnxH28BxnytZdKzg+NKTGj7UhxUUnDD4gpEFcS5Mky33QtXRXiZ42TKy8eC91d7n14ecpbMX9Z+K5n\/NWHrpSTuZdbpfk4GxIKYAO4oJHL6bW9pNeWUSdAH7aV2YIlCkpUUxAjOLUXz\/Cq+LgIJXk+2KdGl+ypelK5nuaGgtgkt0AhePxj55mzitaKzQxeKRGLGkApvZ3Fav4Xnw7Zo2q4R1eXBtvI4VdBOLmUfvjw1OXqusPbxlaw3KnOKy6R36OnoYGIoyVDhi9QhZ2mNMB5C5zIbjijP+acyMcnxVfbVerqCeyYlcZv94qu7RMlzoutNC8qJe8exZphrWkqwkXNSJRdvY98zItYfkIB2pv9krkKwKJJQ7frS6I\/qGaq5p1I0rjQg48zSsCCVGooG\/13TwvYruruBzEcFivl1w2Gq5w8FBjoxxwgv83\/q\/\/tYo3ZKbBjfPRfGOEE20zkaSsgOTzpBS3ExgNVO\/kU3r8Zy54d7H\/OaGrKju+qKTGlsRNJ7Ep91jO0T4Bht96pJedp3EFbEnjUrPnxnDPmYPQgJz2xRmgSzVuOqP9RUuCBW7FAjkXd\/D0Z0HsceW9giMCTrDQ9Nfm6e5WKt595I4WYzsSvt09i8SYUperp6jZ0nfmA53+0qrLX+137Lo4Y\/aZ4Uj6wmrgLY37aDhBvuwahsq7JvsyQGlCHb3v40WYlxHffqtKZJ+2vs4FhyURqyBW0eJypWJJ3CtcP8qfdxQwouseekgyFrszkqXZZVY5dBLdwv1v2YC1ifiqGp+n6n2\/LvGuTeVE7d16NHFgipnXHlDHK+VIHUukkHtcuYe2Jv9fbswEMQiPP+Ymlk0Y\/lZRvzxt\/LsGzr1DNomhfpih8ASDAvxz02AOQMLXE0x1EGH5fFjVrjGJowiVnShwQ442Ht3g3\/jS1ONw\/vtdv6K3PU6YUEuTOuetqmA9XpHnxInNomZec2FUS+NUSlU\/RCxtHNxiPDXL8y5az9\/xF7Aii2Qp3uL+aiuebp33tTInstnJffeENbcEHu2jFI\/n0cDs0FT0H6tbcAdtK+gp\/SYNjfdS2MBiOo4YBENcXBX\/Xo2uzeeEkaw0kQT3RXIsl6eXLBU18p5QwOgzgKbJm\/AB8AYMj9xltbmOxCcj227Q3a9pfMikZFeEHeUykIbQTqg1znb4GiCKbx7Gslyh8bgNnlBuEmAvFetgTXpOnuLZs643PCoNcZEEYRysfkcK+lmixT1raxm4UIdsXJzjM7rHqC0KlGktnIylFWG7qcHkomlDOdLnyQ8D8dObCLu\/6HDAXgMKzspa8BjViku\/doBRu\/WwTMUt4JF+9FksDpc+peqYt7PihmMsWvcn43ctiszjGRrA1gaICW6nZup\/pPPOlcGqgPBXElg+HpU3hh18xDUmUdX5ReFq\/AsPHvCMF8ocqOEeKSysH9Obo8tBgka1l294cYUSZySTg5KX\/9RPTC8bdhlpxxbI54aoS53V9DlAGzHmRwpdvlpQrS78y5l144H3FsGqyX2SYm4eiyhICHr5TU\/mRLpTi8nN0UDOz3w1eEUwtBU2Td76Zt2\/FNqbuNokHDNHtw7Re\/osEPfXw3lw0+rwkBFhkMBA3f30BoKr2MCWcokuelQZZSWhvoxzm34QhgXOafSrEMzV9ElGWIHRBtF29mRupAemHAlzBquiwfUik7DX2Uo8vvIXaxqpnp\/b5WNDm88Q8LAfRgB6EFUCdsniBpTT7BY1hiJ7426Y6ewrAsFGtXMlpEc5XDgcFvZoH\/PEQElhotAQkX+zEug0dquqXsAZVaisO1VIlK6eFN2ALOyEF9NjrTHCx\/ke3xlMCD\/uuJRInOhRkSuGLSSuwyL1hksLDE9z6GeubLX2j9jymP3R0nhSsQDqVzR+d0onLEpbIYd2RcSsPj85g7ozoAFLSglKpO7zvOQPYCqFgvYlXbZLqhOv4CCyt9s\/881mibF0i28FSaDy6vEGn6YlumFNG+UpgR0IRhz5DDKHGLxgu8\/g3P8ccCY5852r+qUSJ0d3L2rGDGRTpJuKxe7a+KogBIIYSpGO\/JB3HfrqQ2GPzyfDOHw9qGGTefcePF8214oTWt7XGGi8tkw1lonGxG0i+CA3P84N7mGxACpLouMTc9qLxtxngXSQ\/H9aXI1VWu3cE\/9lzMZrcQNb97\/zgGuSz9Jgxag+ocYjCpIpH86SJOvyIHAkTzIru7JSnJnDZuYzSyB+AxArdvoEqIxNp9CasXjhJywWAjELWruBB5zTzG\/4IkuGQYPGhqpRzmFvXUz1V5\/SZodhc\/l+DmUg6xbzmr0OhHny4h5\/pEUDIN7njxf2VNgP\/D7LiGaUtnVe79YouaF7MvypSsmKrIoPqapEVaX\/BCObsWyyCrqWS9dWnTmYI+n8ITBxsZWDybRBThkBxhbTik7OscI3WPGpiKMcheFPtw==","iv":"17d5178f7d1903c8f11055c4d7cb043a","s":"bccf0d751b4c01e3"}

The company's latest Signals report lists digital wallets and hyper-personalized checkout experiences among the seven key trends set to transform the sector by 2030. Image credit: Mastercard

The company's latest Signals report lists digital wallets and hyper-personalized checkout experiences among the seven key trends set to transform the sector by 2030. Image credit: Mastercard  The global transaction value of RTP tools is expected to grow from $266 billion in 2023 to $575 billion by 2028. Image credit: Mastercard

The global transaction value of RTP tools is expected to grow from $266 billion in 2023 to $575 billion by 2028. Image credit: Mastercard